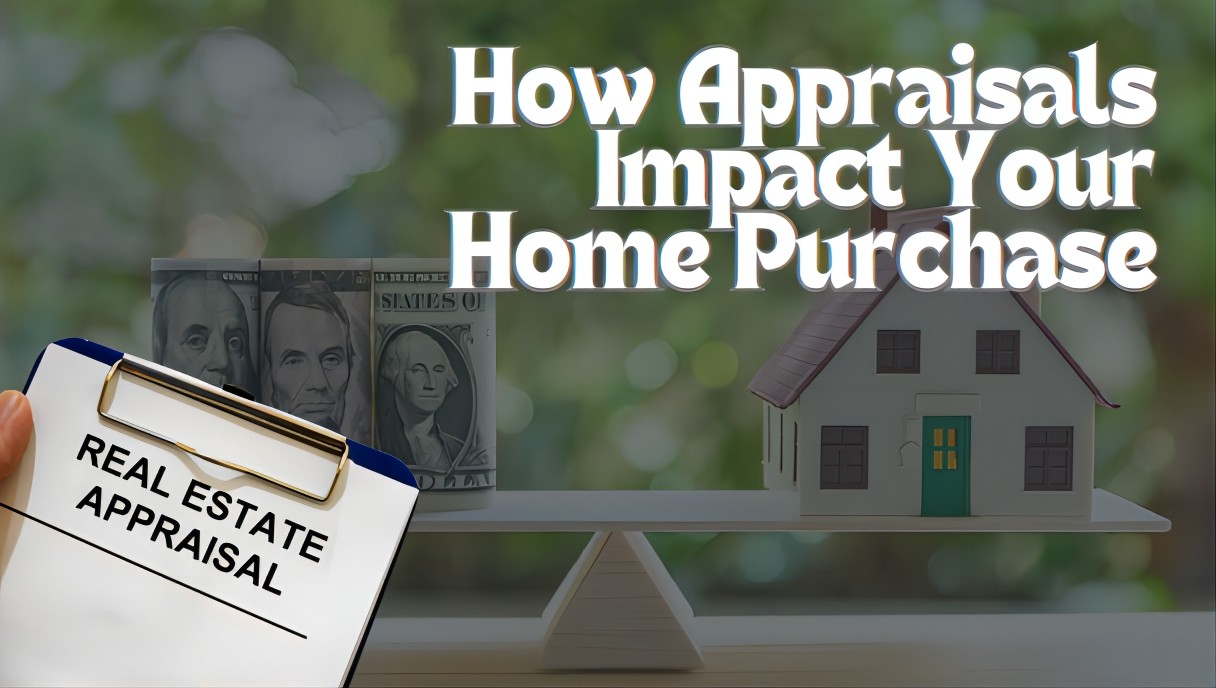

How Appraisals Impact Your Home Purchase

A home appraisal is a critical element in your home purchasing journey. This enables you to make sure that you are getting a fair price for your home.

Normally, before buying your first house, getting a refinance, or taking out a mortgage for your brand new home, you can get it appraised.

If you’re new in the real-estate market, we can guide you through this and explain exactly how appraisals impact your home purchase.

What is a Home Appraisal?

A home appraisal is a non-biased evaluation of your property’s value. A home appraiser is often either determined by the bank (that is financing your home purchase), or an independent but a certified individual.

The appraiser is a real-estate professional who carefully observes the interior and exterior of your home to determine its current value in the market. However, a simple observation isn’t the only requirement for the appraiser.

They also look at the value or the selling price of houses with similar characteristics, to determine what your home might be worth.

How a Home Appraisal can Impact Your Home Purchase?

When an appraiser looks at your home and determines its value, your purchasing journey might look different than what it initially looked like. This depends on whether your home appraisal is higher or lower than the selling price of the house.

To explain this, we have described the two scenarios in detail below to illustrate what both situations could mean for your home purchase.

Scenario 1: Appraisal is higher than the Asking Price

If the appraiser has determined that your home is of a higher value than the selling price, you will have a significant benefit. Because of the appraiser’s evaluation, banks will view the property as a good investment and will view you as lower-risk.

When banks feel their investment is safe, they are more likely to ease up the markup rate on the mortgage.

Hence, you will be able to purchase your home with minimum markup and an easy mortgage. Similarly, you can easily move into your new home by having the reassurance that you bought your house at the right price.

Scenario 2: Appraisal is lower than the Asking Price

Before diving into scenario 2, it is important to note that scenario 1 was the best-case scenario. There is a high probability that the appraisal of your home might be lower than the selling price of the house.

This usually means that the property is worth less than what it is selling for.

As a buyer, you might consider the property expensive in this scenario, especially if you were planning on using cash.

If you had your hopes tied on taking out a mortgage, that might also look like a bad decision. This is because banks will likely charge a higher interest rate for a riskier investment (which in the case of your loan, would be one).

Hence, not only would you have to loan more money, but this might also cost more in the future.

What to do if Your Appraisal Comes in Low?

If your home appraisal comes in lower than the selling price, you might be worrying about the extra expense, or begin questioning your purchasing decision altogether.

It is a reasonable response to worry that the appraisal might cause funding issues in the future. However, this doesn’t mean this is the worst-case scenario.

Lower home appraisals are much more common than people think, especially considering current market conditions. In case your home appraisal is lower than the selling price, it would be useful to renegotiate the price with the seller.

While it may seem like a hassle, a low appraisal value often strengthens your argument and can compel the seller to reconsider their selling price. Due to this, you might end up with a better price for the house and settle in.

If the selling price remains the same, you can also appeal the appraisal value. With your appeal, the appraiser will evaluate your home value once more and can return with a different appraisal value. This is useful if you suspect there were any appraisal errors.

What Does a Home Appraiser Look at?

With the above scenarios in mind, it can be helpful for you to know what a home appraiser looks at to determine the property’s value in the real estate industry.

A home appraiser takes multiple factors into consideration when evaluating the value of a house. This often involves evaluating the interior and the exterior of the house in addition to market-specific factors.

A list of all these factors are listed below for your convenience:

Interior Factors:

●Property Condition

●Number of Rooms

●Property Maintenance

Exterior Factors:

●Property Condition

●Property Size

●Property Location

●Lot Size

●Property Age

Market-Specific Factors:

●Recent sale prices of nearby homes

●Recent sale prices of homes with similar characteristics

How Much do Home Appraisals Cost?

While home appraisal costs can vary a lot considering the property and the appraiser’s pricing structure, a wide range for the cost would be between $400-$2000. Depending on the property size, the home appraisal cost can even be higher than $2000.

How Much Time is Taken for a Home Appraisal?

In the real estate market, a home appraisal doesn't normally take a long time considering that the transaction needs to take place. In most cases, a home appraisal is completed within a timeline of 1-4 weeks.

Who Pays the Home Appraisal Cost?

In the real estate industry, it is common for the buyer to pay for the home appraisal to ensure that they are getting their property for a fair price. In some cases, the seller might offer to pay for the home appraisal as well.

Assess Appraisals with Confidence

A home appraisal is a critical step of the homebuying journey and can affect your home purchasing decision.

It helps you determine the fair value of your property and enables you to buy your dream home at the right price with ease and comfort. With the perfect home, you can begin a new future.

1

1 1

1OTHER NEWS

-

- The Rise of Tech Stocks: Five Key Areas Investors Should Watch

- By Prodosh Kundu 24 Jun,2024

-

- Insuring Your Peace of Mind: An Overview of Common Types of Insurance.

- By Wendy 09 Jun,2023

-

- 5 Ways Traders Can Smartly Invest in Bitcoin

- By Prodosh Kundu 15 May,2024

-

- Understanding Health Insurance: A Guide to Making Informed Decisions!

- By Wendy 24 Apr,2023

-

- Safeguarding Your Rental: A Comprehensive Guide to Renters Insurance!

- By Wendy 04 Jul,2023

-

- It is Best to Consider These Factors When Buying a Home.

- By Wendy 24 Apr,2023

-

- How Appraisals Impact Your Home Purchase

- By Muhammad Talha 16 May,2024

-

- Five Best AI Stocks to Buy

- By Prodosh Kundu 27 Aug,2024

-

- Navigating the Complexities of the Current Housing Market: Trends and Challenges for Buyers and Sellers.

- By Wendy 24 Apr,2023

-

- How US Real Estate Policy Changes Impact Market Performance

- By real estate, policy, finance 20 May,2024

-

- Some Tips on Buying a Condo!

- By Wendy 24 Apr,2023

-

- The Top 5 Fundamentals of Forex Risk Management

- By Prodosh Kundu 13 May,2024